Many regulators around the world seem to think exchanges should be doing cost-based pricing.

As any accountant will know, cost-based pricing isn’t as easy in practice as it seems in theory.

Even the SEC can’t get cost-based pricing to work

Case in point: The U.S. Securities and Exchange Commission (SEC) is operated as an independent federal agency, and its annual costs are paid for using transaction-based fees called Section 31 fees.

The “cost base” of the SEC is pretty simple to calculate. It’s a fairly consistent group of government employees regulating the U.S. securities markets. The agency has a budget that is approved by congress. The costs added to $1.97 billion, according to the 2023 SEC annual report.

From the face of it, this sounds simple. SEC costs are predictable and change pretty slowly.

Yet, the average rate charged varies significantly over time (Chart 1) and even within a year.

Chart 1: The rate of Section 31 fee is volatile (colored by budget cycle)

The main problem is the SEC doesn’t control the “divisor” in its “average costs” calculation.

The agency decided to charge based on value traded. That may be more stable than volumes (shares traded), but it also results in very different costs per trade. In fact, sometimes, for high-priced stocks, it can add to more than a typical mutual fund commission (which is charged in cents-per-share).

Consequently, the “average price” that its accountants budgeted for at the start of the year often needs to be changed – sometimes by a lot. For example, the fee rose from $8 per million dollars traded to $27.8 per million dollars traded in Q2 of 2024 – an increase of almost 350%.

Equal is not fair (or equitable)

These problems affect accountants everywhere.

From an economist’s perspective, it’s impossible to know what the right “divisor” is for creating your average. Is it more economical to charge a variable rate? (And if so, per trade or message or share?) But all of which penalize those who trade a lot and may need economies of scale to be profitable.

The alternative might be a fixed rate per broker (or connection), which might make it difficult for small traders to compete with larger traders.

Both fail to account for economic benefits that perhaps the market should reward. For example, a market maker might trade a lot, and send a lot of messages, leading to a high cost to trade. However, their trading might help set high-quality NBBO that others in the market benefit from (sometimes without even trading on exchange and crossing the spreads that the market makers are setting).

Even with volume tiers, it’s hard for exchanges to reward customers whose activity benefits others in the market. Although ironically (given the SEC’s most recent changes to NMS), rebate markets may do this better than most other solutions – as they pay a rebate to any and all quote-providers – but only on a quote that actually trades.

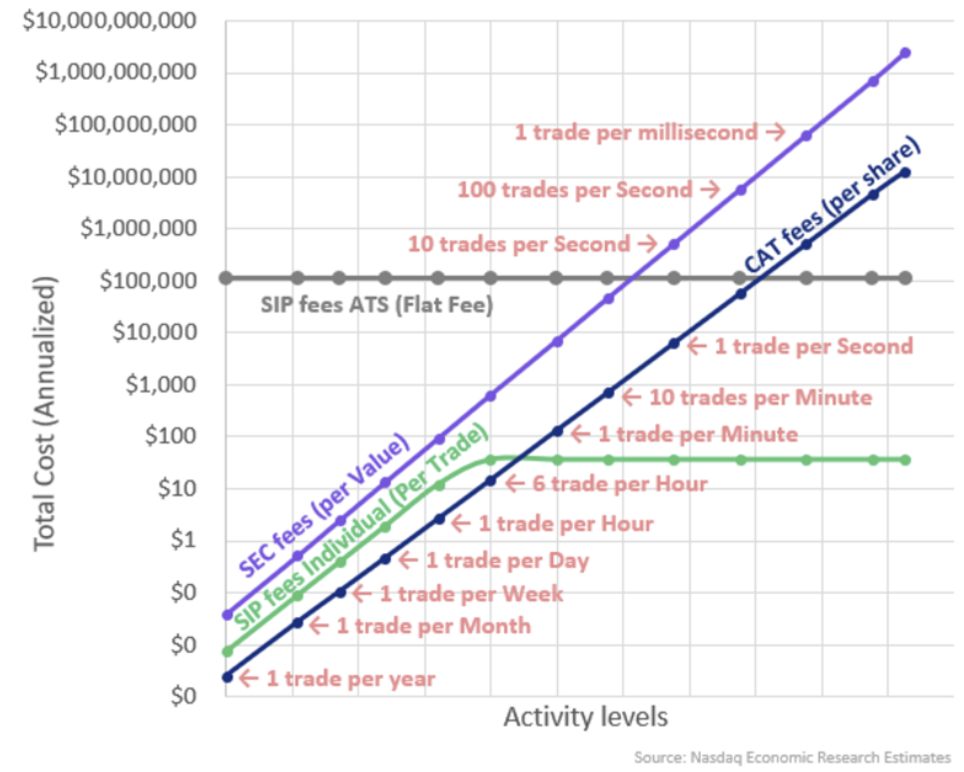

In reality, the U.S. market already has a number of equal solutions. Chart 2 shows that each impacts different kinds of traders differently – noting that even the variable costs are charged based on trades, shares and value. For individuals, there is a fixed base rate of $0.0075 per “view” of the NBBO. For simplicity, in the charts below, we assume that each retail trader views the NBBO only once per trade. Importantly, none of them account for those positive externalities we mentioned above.

Chart 2: There are already multiple attempts to do “equal” fees in the U.S. markets

Platforms make it impossible to allocate costs using rules

Another problem is working out what the “costs” are in the first place.

It could be argued that even the SEC has this problem. The agency has no SEC fee for bond trades or other “securities” that they oversee. That doesn’t imply there are no costs for overseeing them, but it does save the hassle of trying to allocate the costs of the commissioners across each different security and investor type.

Most participants in the global stock markets operate (and compete against) platforms – in that they have more than one product produced by the same process. We can clearly see this when we’ve compared all-in costs to trade. All exchanges charge a different combination of listing, data, connection and trading fees. But we also see different customers drawn to one platform over another because their activity is better suited to a specific fee structure. For example, fading an incoming take order could increase trading profits – even if trading fees of the exchange are higher.

Chart 3: How an exchange splits fees across joint products varies significantly

The same can be seen across brokers.

Some offer execution-only services, others are full-service brokers.

Full-service brokers have higher costs, as they offer services like prime (financing of positions) and research. However, their products are typically bundled into a single commission, which itself is usually “cents per share” cost.

In contrast, execution-only brokers are able to streamline their business model, reducing costs – even though they may potentially compete using lower commissions. Although even those execution-only brokers may choose to pay more for their trading infrastructure in order to differentiate themselves. Adding co-location or faster data feeds should reduce the opportunity costs for their customers, reducing the costs of their trading. That increases their “cost base,” which they may be able to recoup via higher commissions, but that would reduce their cost advantages against full-service brokers.

Of course, not all their customers benefit from these investments in faster trading (or research, or financing). It would seem unfair to force all traders to pay the same commissions.

In almost all industries, it’s bad economics to force all customers to pay the same.

If we really want cost-based pricing – are we willing to support shrinking businesses?

Accounting for, and allocating, costs in the real world is complicated. Cost-based pricing is hard, something even the SEC’s budget process tells us.

Perhaps the most obvious flaw in the “cost-based” argument is this: Should you pay double the original price of the product if half the customers cancel it?

To anyone in the markets that should sound silly — falling demand should make prices fall, not rise — and yet that’s exactly what regulators are supporting when they focus on recovery of costs.